Charitable Lead Trust Frequently Asked Questions

What is a charitable lead trust?

A charitable lead trust (CLT) is designed to accomplish philanthropic objectives at a time when the grantor(s) can take advantage of the high gift and estate tax exemption and reduce exposure to changes in the tax code when the exemption could be lower while providing a gift for Bowdoin (and any other charities supported by the trust) and ensuring that assets remaining in the CLT pass to the next generation in a tax-advantaged way.

Why might a charitable lead trust be appropriate for me?

For people with significant assets, a CLT locks in the ability to take advantage of the high gift and estate exemption to accomplish their philanthropy and ensure assets pass to beneficiaries in a tax-advantaged way.

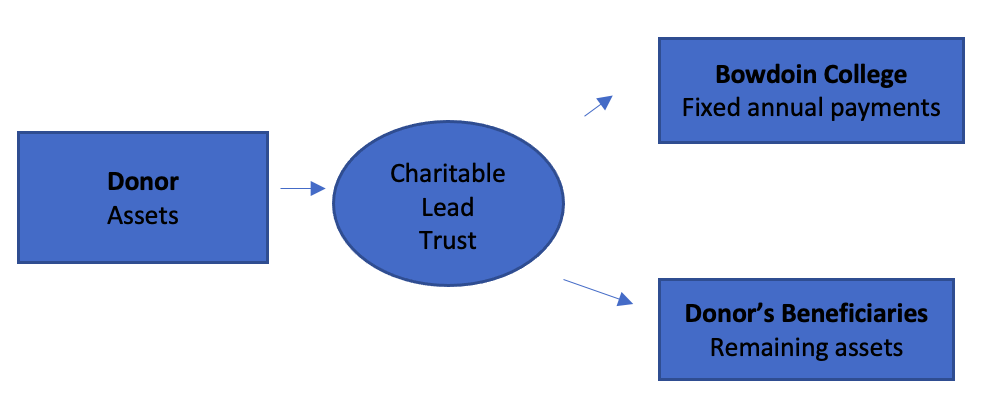

Here is how a CLT works:

- Assets are contributed irrevocably to a trust. You choose the term of the trust and other specifications.

- Your trust makes regular payments to the purpose of your choice at Bowdoin (and sometimes other charities as well).

- When the trust term ends, the remaining assets, including asset appreciation, are paid to your designated beneficiaries.

- The taxable value of the gift to your beneficiaries (if any) is offset by a deduction for the present value of the payments made to Bowdoin (and any other charities supported by the trust).

Case Study

Mr. and Mrs. Smith place $250,000 cash in a non-grantor Charitable Lead Annuity Trust. The CLAT payout rate is optimized to achieve the target gift tax deduction.

The trust will pay 8% of the contribution or approximately $20,000 annually.

The Smiths’ two children will receive the lead trust assets when the trust terminates in 20 years or, at the Smiths' election, the funds remaining in their CLAT can be deployed to fund a new CLAT and/or a life income gift (e.g., a charitable remainder trust).

Result

Beneficiaries (e.g.,children) receive the amount that their parents used to establish the CLAT, $250,000 from the lead trust at its termination assuming annual investment return of 8% (3% annual income and 5% annual appreciation).

Gift tax deduction is $250,000.

Taxable gift to children is $0 which preserves their lifetime gift exclusion.

Over the course of the 20 year trust term, Bowdoin will receive approximately $400,000 from the Smiths’ lead trust.

The total benefit of the Smiths' CLAT is slightly more than $650,000.

The results in this CLAT illustration are based on 4.6 % IRS Discount Rate and may vary due to time of gift and other factors.

How do the people I care about benefit from a CLT?

Your beneficiaries – whether they be your children or other people – enjoy many tax advantages.

- The taxable value of the gift to your beneficiaries is reduced or discounted because they will not actually receive it until sometime in the future.

- All appreciation that takes place in the trust, after the payments to Bowdoin are made, and the remaining assets in the trust passes gift and estate tax-reduced or free to your beneficiaries. Generation-skipping taxes may apply in some situations; however, they can be minimized through careful planning.

Best Assets to Use

- Cash: maximize this low-yield asset

- Stock: high basis

- Interests: in family businesses and/or family limited partnerships

- Income-producing property: with a high appreciation potential (allows eventual transfer to beneficiaries at a low transfer cost)

What are some other opportunities for using a CLT?

In the case of closely-held stock or other business interests, a charitable lead trust offers an opportunity to retain ownership and control within the family. To minimize gift and estate taxes, the lead trust can be used in combination with other estate planning techniques such as a family limited partnership or family dynasty trust.

How can Bowdoin's Office of Gift Planning help?

We are charitable gift planning specialists and have resources available to fully support both your investigation and implementation of gift planning techniques. Our assistance is professional, confidential, collaborative and provided without charge. We encourage you to call on us to provide assistance to you, your family and your advisors in exploring financial, estate and charitable planning. Contact Liz Armstrong in Bowdoin’s Office of Gift Planning.

Charitable Lead Trusts offer many benefits, most notably, the ability to provide annual support for a term of years to charitable organizations you care about and the opportunity to pass assets to the next generation in a tax-advantaged way. The IRS discount rate is a critical factor in valuing future gifts to a charitable institution over a period of years. The Case Study illustrates how a charitable lead trust can significantly reduce the tax liability on the assets transferred into the lead trust.

Gift and estate tax exemption amounts are high but may not be in the future. Moving assets into a Charitable Lead Trust to accomplish philanthropic objectives may be a good strategy to move them out of one's estate and provide for the CLT remainder to pass in a tax-advantaged way directly to beneficiaries at the end of the CLT term.

Drafting CLT terms is not complicated. The IRS has sample templates for your advisors to use. You can access a sample of an inter vivos Charitable Lead Annuity Trust by clinching here. For a sample of a testamentary Charitable Lead Annuity Trust, click here.

Please note that we are prohibited from giving legal or financial advice and none of the information above should be interpreted as such. We encourage you to consult with your own legal counsel or financial advisor before deciding whether or not to proceed with a gift.